REFERRAL PERKS®

Earn $100* for you and your friend for every successful referral.

It is an age-old question. One that has troubled countless Canadians for decades. As the market shifts, the question is becoming even more important. The answer is not simple, and not the same for every Canadian.

The renting and buying debates are about more than just finances. With housing markets and rents setting unprecedented levels, it is not only about having a down payment. It depends on your lifestyle, current financial situation, and your long-term goals.

Over the past few years, several things have changed. There has been an uptick in remote work and shifts in the global economy that many are taking into consideration as they consider making the leap to home ownership.

Owning a home is a landmark event. It is an important decision that is often the result of a lot of hard work.

There is a lot to consider as you start to weigh out your options for home-ownership. Be sure to weigh the pros and cons for renting and buying and make a decision that sets you up for success, now and in the future.

Buying

Renting

The questions that most people often wonder are:

Questions that you should be asking include:

With rising house costs, buying might feel like a challenge. It also might not feel realistic to save for a down payment. It might not be easy, but there are ways that you can increase your savings to get into the housing market.

If you are living in a two-bedroom condo, you could re-evaluate and get a one-bedroom or two-bedroom in a purpose-built rental. A purpose-built rental is a unit in a privately initiated structure of three units or more, typically they are apartments or row houses.

Rent your extra space

If you have a partner or live on your own, you could consider getting a roommate to help with the cost of renting. Use their contribution towards your down payment!

Analyze your household expenses

Every dollar saved helps in your journey to homeownership. Create a budget and stick to it. Look for alternatives for utility bills, phone bills and subscriptions. With a few simple lifestyle shifts, you could be saving like a pro.

Boost your savings

Take a look at your savings accounts. Are you maximizing your return potential? Are you working with a financial professional that can guide you on the best investments such as GICs / term deposits?

Take advantage of our Home Sweet Bonus® account, if you’re thinking of buying in the next few years, you could earn up to $1000 on us*.

It is important to ensure you are saving effectively and using all the programs available to first-time homebuyers as you start looking for a home and calculate how much you need for a down payment and monthly mortgage payments. Don’t guess! Use our mortgage calculator to estimate how much you may be able to borrow and what your monthly payments might be.

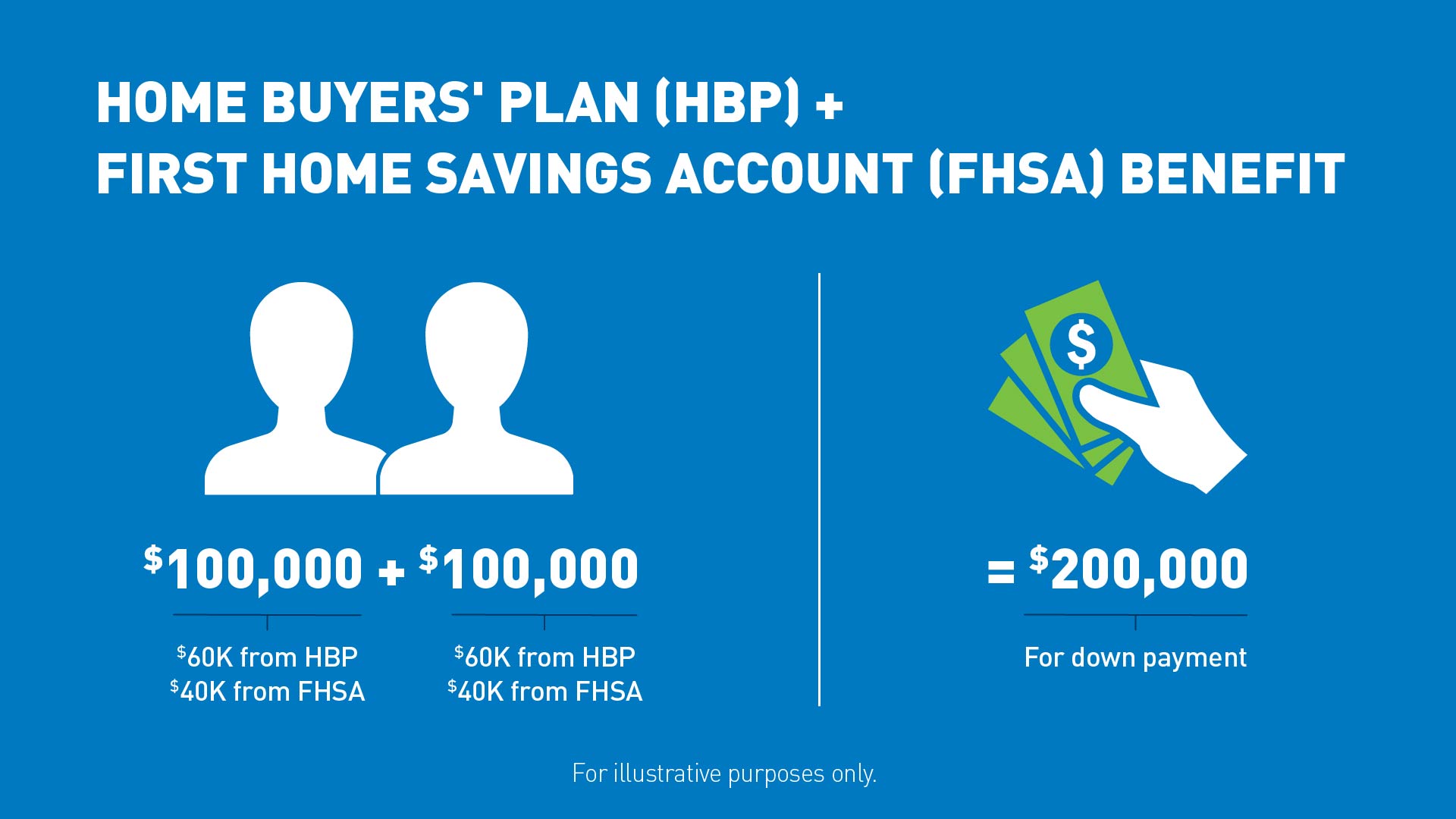

Make the most of your Tax-Free Savings Account (TFSA) and Registered Retirement Savings Plan (RRSP), which has the added bonus in Canada of the Home Buyers Plan (HBP). Through the HBP, you can lend yourself up to $60,000 (or $120,000 if your buying partner has never owned a home before) tax-free!

In 2022, the Canadian government introduced the First Home Savings Accounts (FHSA) to assist eligible Canadian residents in buying their first home. With an FHSA, you can add up to $40,000 tax-free to your savings; that's in addition to the $60,000 contribution limit on the HBP, meaning you can save up to $100,000 tax-free for your first home.

After you have determined how much of your savings can support your down payment, you might consider speaking to family members who may help by gifting some money. There is no gift tax in Canada and no limit on the amount that can be given. It is not taxable as income or deductible as an expense.

Unfortunately, there is no definitive answer to this question, it will depend on your situation and where you currently are in both your life and career. However, an advisor can help set you up to make the most out of your current income and savings. Having a good understanding of your financial situation may help you answer the question, should I rent or buy?

Get the financial advice you need

You don't have to figure out a plan on your own. Work with an advisor to find solutions that support your financial goals.

*Terms and conditions apply. Please visit Home Sweet Bonus® for more details.

You are solely responsible for confirming that your FHSA, TFSA and RRSP contributions are within your allowable limits set by Canada Revenue Agency (CRA). All rules and contribution limits for FHSAs are set out by CRA and applicable legislation apply. Information about FHSAs is based on what is currently available from the Canadian government and may be subject to change.

Financial planning services are available only from advisors who hold financial planning accreditation from applicable regulatory authorities. Mutual funds and other securities are offered through Aviso Wealth, a division of Aviso Financial Inc.

Speak to an advisor on the phone or at a branch.

We acknowledge that we have the privilege of doing business on the traditional territory of First Nations communities.