REFERRAL PERKS®

Earn $100* for you and your friend for every successful referral.

You’ve been doing your research, watching the housing market and saving for a down payment. It’s been years in the making and you can’t wait for the moment when you walk through the door and know ‘this will be my home.’ There is nothing more exciting than having your offer accepted and knowing you are home.

As you’ve been watching the market, you might be questioning the affordability of buying a house.

Some questions might include:

These are important questions and ones that need to be answered before you find, a place to call “home sweet home.”

In general, it's recommend that a house payment is under 32% of your gross monthly income. This includes the mortgage payment, maintenance costs and property taxes. For example, if your monthly income is $5,000, or $60,000 a year, your mortgage payment should not exceed $1,500 each month. Use our mortgage calculator to find out more about how much you can borrow and what your monthly payments will be.

When you apply for a mortgage, the lender looks at a lot of factors beyond your income to determine the amount they will lend you. They will look at your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. These ratios determine how easily your income can support your debts and other financial obligations.

You may have also heard about the need to pass a mortgage stress test.

The Canadian Government requires borrowers to pass this stress test to prove you can afford your mortgage payments at a qualifying interest rate, which is typically higher than the actual interest rate of your mortgage and will likely reduce the mortgage amount you will qualify for. That’s because your ability to make repayments will be measured against the qualifying rate set by the Bank of Canada and not the rate charged by your lender. Anyone looking to purchase a new purchase, refinance a home, switch to a new lender, or take out a home equity line of credit will need to pass the stress test.

However, the amount you can afford to carry each month is only part of the equation. A big step to owning a home is having a down payment.

When buying a house, you need an initial payment against the total price of the home, this is referred to as the down payment. In Canada, the minimum down payment is five percent of the purchase price.

| Purchase price | Minimum down payment |

| Up to $500,000 |

|

| Between $500,000 and $1,499,999 |

|

| $1,500,000 and over |

|

*According to the Financial Consumer Agency of Canada

If your down payment is less than 20% of the total purchase price, you are required to get mortgage loan insurance through the government-owned housing agency called the Canada Mortgage and Housing Corporation (CMHC), Sagen or Canada Guaranty Mortgage Insurance Company.

The mortgage insurance premium is different depending on many factors including:

Overall, the higher the percentage of the total house price that you borrow, the higher insurance premium you will have to pay.

This all leads to the question:

How do you save for a down payment and what are your options for increasing the amount you put down so you can carry less of a mortgage and pay less insurance?

You might be surprised at the amount of money Canadian home buyers are receiving for down payments. According to current Canadian law, parents can give cash gifts with no limit. If the gift is in the form of a property that is not a parent’s principal residence, it will be taxed through capital gains. The capital gains tax is based on the fair market value from the date it was gifted.

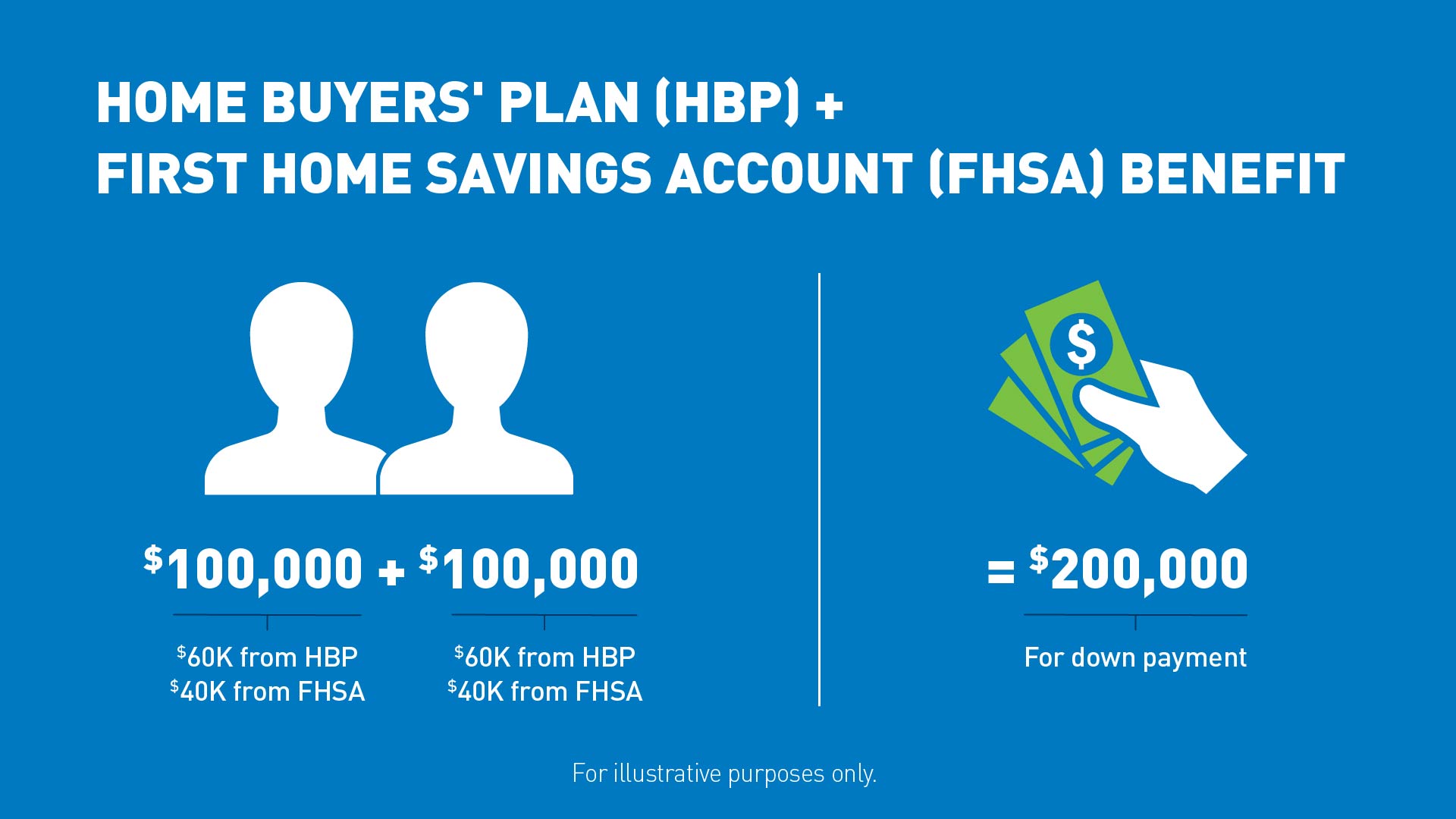

Before calling your real estate agent, have an idea of your affordability both for your mortgage and down payment. Put together all your saving sources to understand your full financial picture. Talk to family about any cash they may gift you. If it's an option you may need to decide how much to pull from your Tax-Free Savings Account (TFSA) and Registered Retirement Savings Plan (RRSP), which has the added bonus in Canada of the Home Buyers Plan. This plan allows first-time buyers in Canada to lend themselves up to $60,000 tax-free dollars from their Registered Retirement Savings Plan (RRSP). An extra bonus is you don’t have to start paying it back for two years and then you have a 15-year repayment period.

To help boost your savings, you may be eligible for our Home Sweet Bonus® Account if you’re looking to buy in the next one to three years. This account provides an incentive to save a minimum of $100 a month until you’re ready to get a mortgage with us, and we’ll add a bonus of up to $1,000* to help with your mortgage down payment. This is a great option to help you save more of your own money, meaning you won’t have to pay back any of your contributions.

Get the financial advice you need

You don't have to figure out a plan on your own. Work with an advisor to find solutions that support your financial goals.

*Terms and conditions apply. Please visit Home Sweet Bonus® for more details.

You are solely responsible for confirming that your FHSA, TFSA and RRSP contributions are within your allowable limits set by Canada Revenue Agency (CRA). All rules and contribution limits for FHSAs are set out by CRA and applicable legislation apply. Information about FHSAs is based on what is currently available from the Canadian government and may be subject to change.

Financial planning services are available only from advisors who hold financial planning accreditation from applicable regulatory authorities. Mutual funds and other securities are offered through Aviso Wealth, a division of Aviso Financial Inc.

Speak to an advisor on the phone or at a branch.

We acknowledge that we have the privilege of doing business on the traditional territory of First Nations communities.